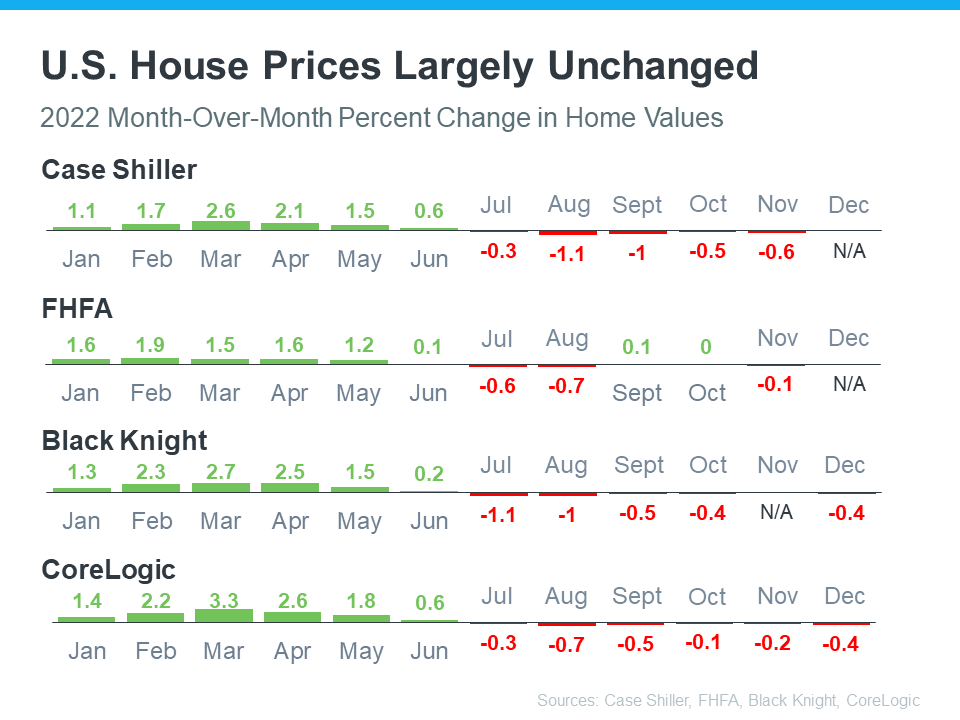

The recent changes in home prices are top of mind for many as the housing market begins gearing up for spring. It can be hard to navigate misleading headlines and confusing data, so here’s what you should know about today’s home prices. Local price trends still vary by market. But looking at national data, Nataliya Polkovnichenko, Ph.D., Supervisory Economist at the Federal Housing Finance Agency (FHFA), explains: “U.S. house prices were largely unchanged in the last four months and remained near the peak levels reached over the summer of 2022. While higher mortgage rates have suppressed demand, low inventories of homes for sale have helped maintain relatively flat house prices.” Month-over-month home price changes can be seen in the chart below. The data also shows that price depreciation peaked around August. Since then, any depreciation has been even milder. In other words, today’s home prices aren’t in a freefall.  What Does This Mean for You? If you currently own your house, you may be concerned about even the smallest decline in prices. But keep in mind how much home values grew over the last few years. Compared to that growth, any declines we’re seeing nationally are likely to be minimal. Selma Hepp, Chief Economist at CoreLogic, shares: “. . . while prices continued to fall from November, the rate of decline was lower than that seen in the summer and still adds up to only a 3% cumulative drop in prices since last spring’s peak.” It’s also important to remember that every local market is different. That’s why it’s essential to lean on an expert for the latest information on the home prices in your area if you’re planning to make a move this spring. Bottom Line To understand what’s going on with home prices in our market and how they could impact your goals, let’s connect today.

0 Comments

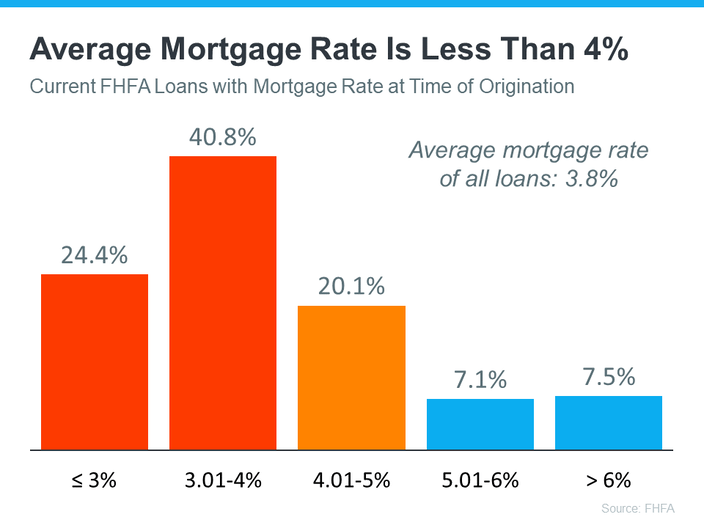

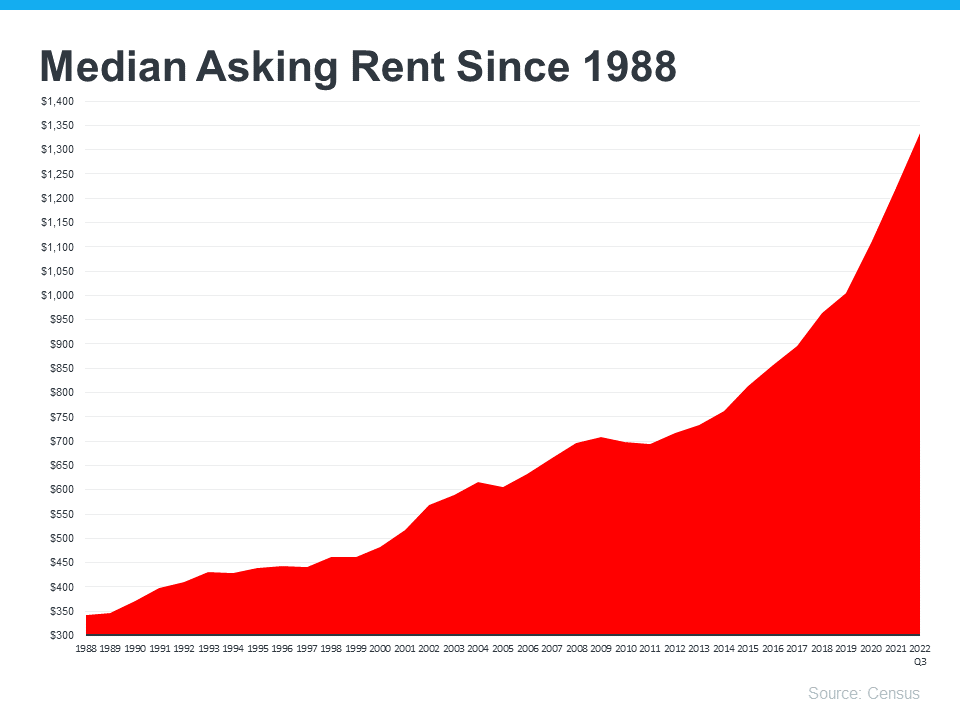

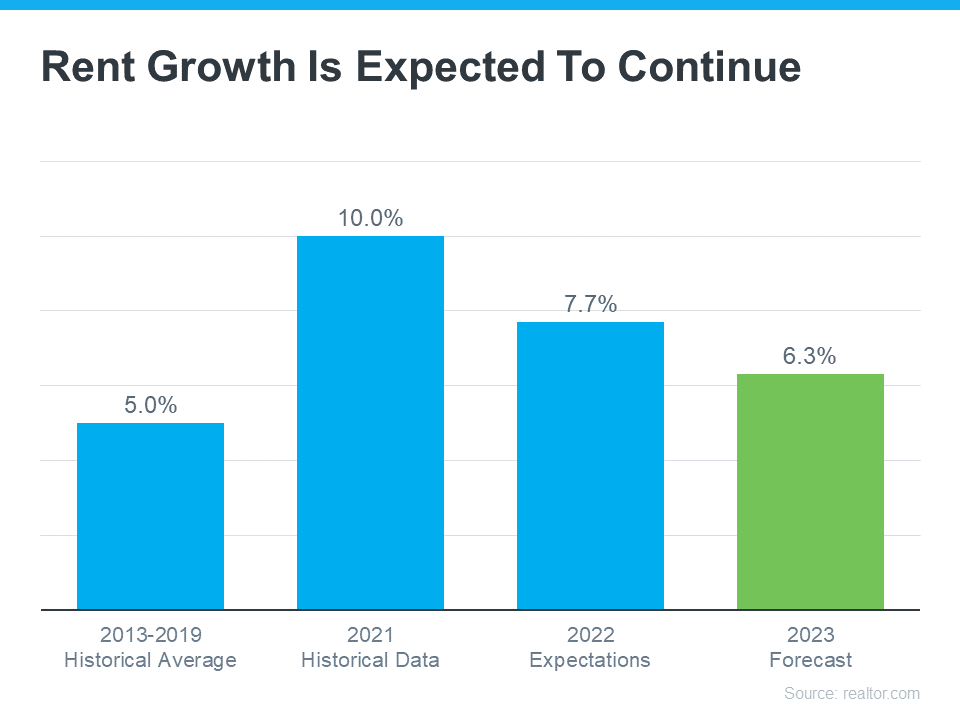

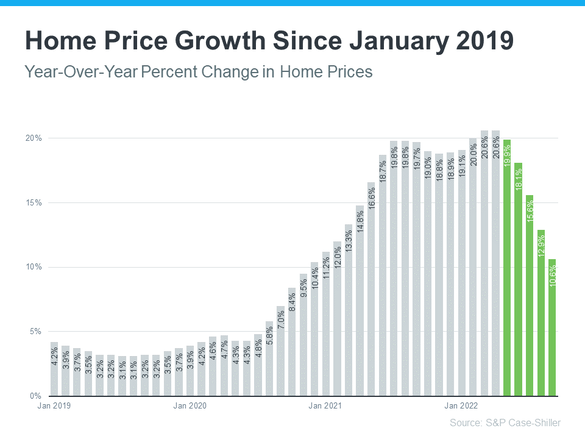

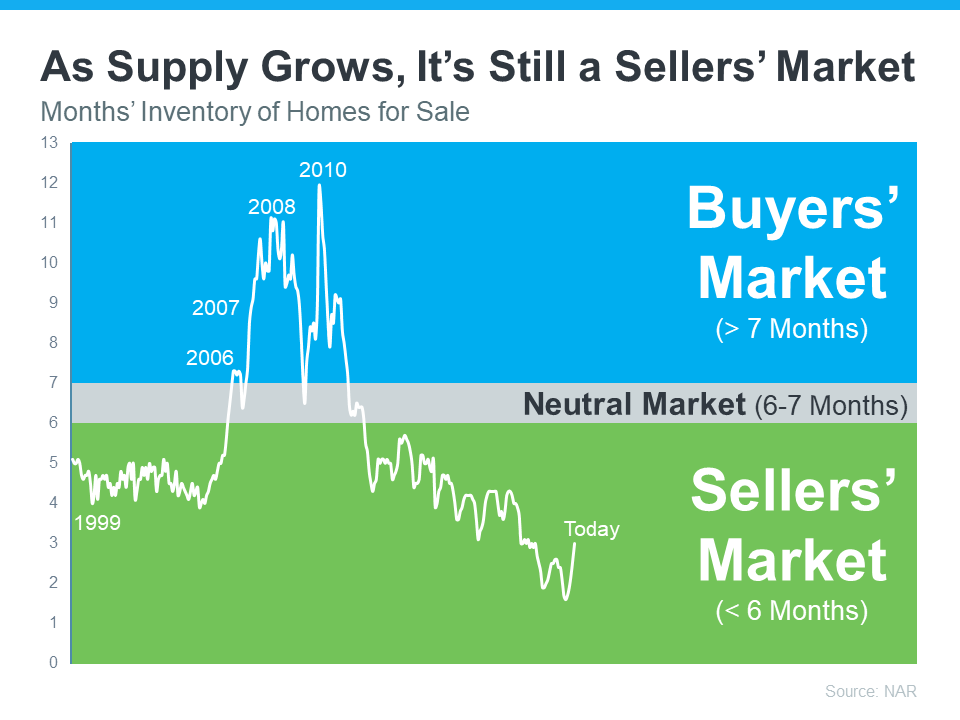

The biggest challenge the housing market’s facing is how few homes there are for sale. Mark Fleming, Chief Economist at First American, explains the root causes of today’s low supply: “Two dynamics are keeping existing-home inventory historically low – rate-locked existing homeowners and the fear of not finding something to buy.” Let’s break down these two big issues in today’s housing market. Rate-Locked Homeowners According to the Federal Housing Finance Agency (FHFA), the average interest rate for current homeowners with mortgages is less than 4% (see graph below):  But today, the typical mortgage rate offered to buyers is over 6%. As a result, many homeowners are opting to stay put instead of moving to another home with a higher borrowing cost. This is a situation known as being rate locked. When so many homeowners are rate locked and reluctant to sell, it’s a challenge for a housing market that needs more inventory. However, experts project mortgage rates will gradually fall this year, and that could mean more people will be willing to move as that happens. The Fear of Not Finding Something To Buy The other factor holding back potential sellers is the fear of not finding another home to buy if they move. Worrying about where they’ll go has left many on the sidelines as they wait for more homes to come to the market. That’s why, if you’re on the fence about selling, it’s important to consider all your options. That includes newly built homes, especially right now when builders are offering concessions like mortgage rate buydowns. What Does This Mean for You? These two issues are keeping the supply of homes for sale lower than pre-pandemic levels. But if you want to sell your house, today’s market is a sweet spot that can work to your advantage. Be sure to work with a local real estate professional to explore the options you have right now, which could include leveraging your current home equity. According to ATTOM: “. . . 48 percent of mortgaged residential properties in the United States were considered equity-rich in the fourth quarter, meaning that the combined estimated amount of loan balances secured by those properties was no more than 50 percent of their estimated market values.” This could make a major difference when you move. Work with a local real estate expert to learn how putting your equity to work can keep the cost of your next home down. Bottom Line Rate-locked homeowners and the fear of not finding something to buy are keeping housing inventory low across the country. But as mortgage rates start to come down this year and homeowners explore all their options, we should expect more homes to come to the market.  If you’re a renter, you likely face an important decision every year: renew your current lease, start a new one, or buy a home. This year is no different. But before you dive too deeply into your options, it helps to understand the true costs of renting moving forward. In the past year, both current renters and new renters have seen their rent go up based on information from realtor.com: “Three out of four renters (74.2%) who have moved in the past 12 months reported seeing their rent increase. The strain from recent rent hikes isn’t exclusive to renters who have recently moved. Nearly two-thirds of renters (63.2%) who have lived in their current rental between 12 and 24 months, and likely renewed their lease, have also reported increases in their rent.” And if you look back at historical data, that shouldn’t come as surprise. That’s because, according to the Census, rents have been rising fairly consistently since 1988 (see graph below):  So, if you’re considering renting as an option in 2023, it’s worth weighing whether this trend is likely to continue. The 2023 Housing Forecast from realtor.com expects rents will keep climbing (see graph below):  That forecast projects rents will increase by 6.3% in the year ahead (shown in green). When compared to the blue bars in the graph, it’s clear that the 2023 projection doesn’t call for an increase as drastic as the ones renters have seen over the past two years, but it’s still above the historical average for rent hikes between 2013-2019. That means, if you’re planning to rent again this year and you’ve not yet renewed your lease, you may pay more when you do. Homeownership Provides an Alternative to Rising Rents These rising costs may make you reconsider what other alternatives you have. If you're looking for more stability, it could be time to prioritize homeownership. One of the many benefits of owning your own home is it provides a stable monthly cost that you can lock in for the duration of your loan. As Freddie Mac says: “Monthly rent payments may increase over time, but a fixed-rate mortgage will ensure that you're paying the same amount each month. With a fixed-rate mortgage, your interest rate is locked in for the life of loan. Steady payments allow you to budget wisely and make plans for the future.” If you’re planning to make a move this year, locking in your monthly housing costs for the duration of your loan can be a major benefit. You’ll avoid wondering if you’ll need to adjust your budget to account for annual increases like you would if you left your housing payment up to your landlord and their renewal cycle. Homeowners also enjoy the added benefit of home equity, which has grown substantially. In fact, the latest Homeowner Equity Insight report from CoreLogic shows the average homeowner gained $34,300 in equity over the last 12 months. As a renter, your rent payment only covers the cost of your dwelling. When you pay your mortgage on a house, you grow your wealth through the forced savings that is your home equity. Bottom Line If you’re thinking of renting this year, it’s important to keep in mind the true costs you’ll face. Let’s chat to see how you can begin your journey to homeownership today.  If you’re trying to decide whether or not to sell your house, recent headlines about home prices may be top of mind. And if those stories have you wondering what that means for your home’s value, here’s what you really need to know. What’s Really Happening with Home Prices? It’s possible you’ve seen news stories mentioning a drop in home values or home price depreciation, but it’s important to remember those headlines are designed to make a big impression in just a few words. But what headlines aren’t always great at is painting the full picture. While home prices are down slightly month-over-month in some markets, it’s also true that home values are up nationally on a year-over-year basis. The graph below uses the latest data from S&P Case-Shiller to help tell the story of what’s actually happening in the housing market today:  As the graph shows, it’s true home price growth has moderated in recent months (shown in green) as buyer demand has pulled back in response to higher mortgage rates. This is what the headlines are drawing attention to today. But what’s important to notice is the bigger, longer-term picture. While home price growth is moderating month-over-month, the percent of appreciation year-over-year is still well above the home price change we saw during more normal years in the market. The bars for January 2019 through mid-2020 show home price appreciation around 3-4% a year was more typical (see bars for January 2019 through mid-2020). But even the latest data for this year shows prices have still climbed by roughly 10% over last year. What Does This Mean for Your Home’s Equity? While you may not be able to capitalize on the 20% appreciation we saw in early 2022, in most markets your home’s value, on average, is up 10% over last year – and a 10% gain is still dramatic compared to a more normal level of appreciation (3-4%). The big takeaway? Don’t let the headlines get in the way of your plans to sell. Over the past two years alone, you’ve likely gained a substantial amount of equity in your home as home prices climbed. Even though home price moderation will vary by market moving forward, you can still use the boost your equity got to help power your move. As Mark Fleming, Chief Economist at First American, says: “Potential home sellers gained significant amounts of equity over the pandemic, so even as affordability-constrained buyer demand spurs price declines in some markets, potential sellers are unlikely to lose all that they have gained.” Bottom Line If you have questions about home prices or how much equity you have in your current home, let’s connect so you have an expert’s advice.  If you’re thinking about buying or selling a home this year, you may have questions about what’s happening with home prices today as the market cools. In the simplest sense, nationally, experts don’t expect prices to come crashing down, but the level of home price moderation will depend on factors like supply and demand in each local market. That means, moving forward, home price appreciation will continue to vary by location, with more significant changes happening in overheated areas. Here’s a quick snapshot of what the experts are saying: Danielle Hale, Chief Economist at realtor.com, says: “The major question on the minds of homeowners and aspiring buyers alike is what will happen to home prices. . . Soaring prices were propelled by all-time low mortgage rates which are a thing of the past. As a result, home price growth is expected to continue slowing, dipping below its pre-pandemic average to 5.4% for 2023, as a whole.” Mark Fleming, Chief Economist at First American, says: “House price appreciation has slowed in all 50 markets we track, but the deceleration is generally more dramatic in areas that experienced the strongest peak appreciation rates.” Taylor Marr, Deputy Chief Economist at Redfin, says: “For those bearish folks eagerly awaiting the home price crash, you’ll have to keep waiting. As much as demand is pulling back supply is as well reducing downward pressure on prices in the short run.” John Paulson, Founder of Paulson & Co., says: “It’s true – housing may be a little frothy. So housing prices may come down or they may plateau . . .” What Does This Mean for You? The best way to get the answers you need is to lean on a local real estate advisor. They’ll be able to explain the latest trends in your specific market so you can make a confident and informed decision on your next step toward buying or selling a home. Bottom Line If you have questions about what’s happening with home prices today, let’s connect so you have the latest on our local market. Welcome to your new home in Queensview! Perched on the 14th floor at 21-25 34th Avenue, discover apartment #14C, a spacious three-bedroom sanctuary boasting breathtaking vistas of Astoria and Long Island City. Revel in the beauty of northeastern-facing sunrises that greet you each morning as you step onto the wood-floored haven, complete with one and a half baths for added convenience. With sweeping panoramas from every room, immerse yourself in the charm of this expansive unit that promises a lifestyle of comfort and delight. Queensview, a residential cooperative housing complex spanning the border of Astoria and Long Island City, offers more than just a home; it presents a community-oriented haven spread across 10 acres of lush greenery. Embrace the ease of on-site laundry facilities in each of the 14 buildings, alongside the option for outdoor parking and the added amenities of a playground and basketball court, perfect for leisurely afternoons or energetic play. Convenience meets culture with Queensview's prime location, mere moments from Astoria's eclectic array of bars, restaurants, and boutiques. Commuting into Manhattan is a breeze with the nearby Broadway Station (N & W trains), while seamless access to major thoroughfares including the Triboro Bridge, 59th Street Bridge, midtown tunnel, and LIE ensures effortless travel throughout the city and beyond. Please note that while the refrigerator and dishwasher seen in the images have been recently removed at the request of management and are not included in the sale, the allure of Queensview's cat-friendly environment beckons you to make this space your own. All showings and Open Houses are available by Appointment only, ensuring a personalized experience tailored to your needs. For further information or to schedule a viewing, contact Colin O'Leary at 646-300-2012 and embark on your journey to Queensview living today.  There’s no denying the housing market is undergoing a shift this season, and that may leave you with some questions about whether it still makes sense to sell your house. Here are three of the top questions you may be asking – and the data that helps answer them – so you can make a confident decision. 1. Should I Wait To Sell? Even though the supply of homes for sale has increased in 2022, inventory is still low overall. That means it’s still a sellers’ market. The graph below helps put the inventory growth into perspective. Using data from the National Association of Realtors (NAR), it shows just how far off we are from flipping to a buyers’ market:  While buyers have regained some negotiation power as inventory has grown, you haven’t missed your window to sell. Your house could still stand out since inventory is low, especially if you list now while other sellers hold off until after the holiday rush and the start of the new year. 2. Are Buyers Still Out There? If you’re thinking of selling your house but are hesitant because you're worried buyer demand has disappeared in the face of higher mortgage rates, know that isn’t the case for everyone. While demand has eased this year, millennials are still looking for homes. As an article in Forbes explains: “At about 80 million strong, millennials currently make up the largest share of homebuyers (43%) in the U.S., according to a recent National Association of Realtors (NAR) report. Simply due to their numbers and eagerness to become homeowners, this cohort is quite literally shaping the next frontier of the homebuying process. Once known as the ‘rent generation,’ millennials have proven to be savvy buyers who are quite nimble in their quest to own real estate. In fact, I don’t think it’s a stretch to say they are the key to the overall health and stability of the current housing industry.” While the millennial generation has been dubbed the renter generation, that namesake may not be appropriate anymore. Millennials, the largest generation, are actually a significant driving force for buyer demand in the housing market today. If you’re wondering if buyers are still out there, know that there are still people who are searching for a home to buy today. And your house may be exactly what they’re looking for. 3. Can I Afford To Buy My Next Home? If current market conditions have you worried about how you’ll afford your next move, consider this: you may have more equity in your current home than you realize. Homeowners have gained significant equity over the past few years and that equity can make a big difference in the affordability equation, especially with mortgage rates higher now than they were last year. According to Mark Fleming, Chief Economist at First American: “. . . homeowners, in aggregate, have historically high levels of home equity. For some of those equity-rich homeowners, that means moving and taking on a higher mortgage rate isn’t a huge deal—especially if they are moving to a more affordable city.” Bottom Line If you’re thinking about selling your house this season, let’s connect so you have the expert insights you need to make the best possible move today.  For over 78 years, Veterans Affairs (VA) home loans have provided millions of veterans with the opportunity to purchase homes of their own. If you or a loved one have served, it’s important to understand this program and its benefits.

Here are some things you should know about VA loans before you start the homebuying process. What Are VA Loans? VA home loans provide a pathway to homeownership for those who have served our nation. The U.S. Department of Veterans Affairs describes the program like this: “VA helps Servicemembers, Veterans, and eligible surviving spouses become homeowners. As part of our mission to serve you, we provide a home loan guaranty benefit and other housing-related programs to help you buy, build, repair, retain, or adapt a home for your own personal occupancy.” Top Benefits of the VA Home Loan Program In addition to helping eligible buyers achieve their homeownership dreams, VA loans have several other great benefits for buyers who qualify. According to the Department of Veteran Affairs:

A recent article from Veterans United sums up just how impactful this loan option can be: “For the vast majority of military borrowers, VA loans represent the most powerful lending program on the market. These flexible, $0-down payment mortgages have helped more than 24 million service members become homeowners since 1944.” John Bell, Acting Executive Director of the Department of Veterans Affairs Loan Guaranty Service, also explains why this program is so powerful: “It provides early ownership for many people that would not have that opportunity to begin with. Since there’s no down payment, it allows people to hold their wealth and it gives them the ability to have long term financial security by being able to own a house and let that equity grow.” Bottom Line Homeownership is the American Dream. Our veterans sacrifice so much in service of our nation, and one way we can honor and thank them is to ensure they have the best information about the benefits of VA home loans. Thank you for your service. |

BLOG Archives

April 2024

|

|

The Big City Team

Berkshire Hathaway HomeServices 6416 Bay Parkway, 2nd floor Brooklyn, New York 11204 Colin R. O'Leary Founder & Team Leader Licensed R.E. Salesperson Phone: 646-300-2012 Email: colinoleary@bhhsfillmore.com |

|

Your Trusted Partners in Real Estate Across the NYC Metro Area

© 2024 BHH Affiliates, LLC. An independently owned and operated franchisee of BHH Affiliates, LLC.

Berkshire Hathaway HomeServices and the Berkshire Hathaway HomeServices symbol are registered service marks of Columbia Insurance Company, a Berkshire Hathaway affiliate.

Equal Housing Opportunity.

Privacy Policy