Moving to New York City can be an exciting and life-changing decision, but it's also a significant step that comes with its own set of challenges and considerations. Here are seven compelling reasons why people are choosing to move to NYC:

However, it's essential to consider the high cost of living, including housing, in NYC. Rent and real estate prices can be exceptionally high, and the city's fast-paced lifestyle may not be for everyone. Additionally, NYC's climate, with hot summers and cold winters, may not suit everyone's preferences. Before making the move, it's crucial to research thoroughly, plan your finances, and visit the city to get a feel for what life in NYC is really like. NYC offers many opportunities and experiences, but it's essential to make an informed decision based on your individual priorities and circumstances. If you're planning to move to NYC, contact The Big City Team at 646-300-2012 to schedule free consultation.

0 Comments

Generation Z (Gen Z) is eager to put down their own roots and achieve financial independence. As a result, they’re turning to home ownership. According to the latest Home Buyers and Sellers Generational Trends Report from the National Association of Realtors (NAR), 30% of Gen Z buyers transitioned straight from living under their parents' roofs to owning their own homes. If you’re a member of this generation, and you’re interested in pursuing your own dream of home ownership, here’s some information you may find helpful on why and where your peers are buying. The Reasons Gen Z Want To Become Homeowners A recent survey by Rocket Mortgage identifies some of the top motivators driving Gen Z buyers to purchase a home: “Of those surveyed, 34% said that starting or growing their family was their main motivation to buy a home. . . . Along with growing a family comes establishing a home base.” Another key reason the survey says Gen Z wants to buy is because home ownership can give them more stability (20.8%). That’s because buying a home allows you to stabilize what’s typically your biggest monthly expense: your housing cost. When you have a fixed-rate mortgage on your home, you can lock in your monthly payment for the duration of your loan, often 15 to 30 years. If you keep renting, you don’t have that same benefit, and you won’t be protected from rising housing costs. So, if you’re ready to start a new chapter in your life or if you’re craving more stability, know that your peers feel the same way, and those motivators are why they’re turning to home ownership. Gen Z's Next Stop: Where Are They Making Their Moves? If those reasons have you feeling ready to buy, here’s some information on where your peers are finding their homes that could help you with your search. According to a recent Lending Tree survey, Gen Z buyers are focusing on more affordable areas to help boost their buying power and offset the challenges that come with today’s mortgage rates. Many Gen Z buyers still want the convenience and excitement of city life, but also value the affordability, open air, and space more suburban areas offer. Jacob Channel, Senior Economist at LendingTree, explains: “. . . they want to live in a city, but they also want to be close to nature.” Locating a home that offers both of those things requires expertise. Working with a trusted real estate professional can help you find a home in your budget and desired area. Your agent will know the most affordable neighborhoods to search in. They can also highlight the amenities and features that location offers and how those are aligned with your goals. They’ll also be able to walk you through how things like remote work can help you cast a broader net for your search. Bottom Line If you’re a member of Gen Z and are just getting started on your home buying journey, or if you want to learn more about the process, let’s connect. That way, you have a guide to help you find a home that fits both your lifestyle and your budget.  Some Highlights

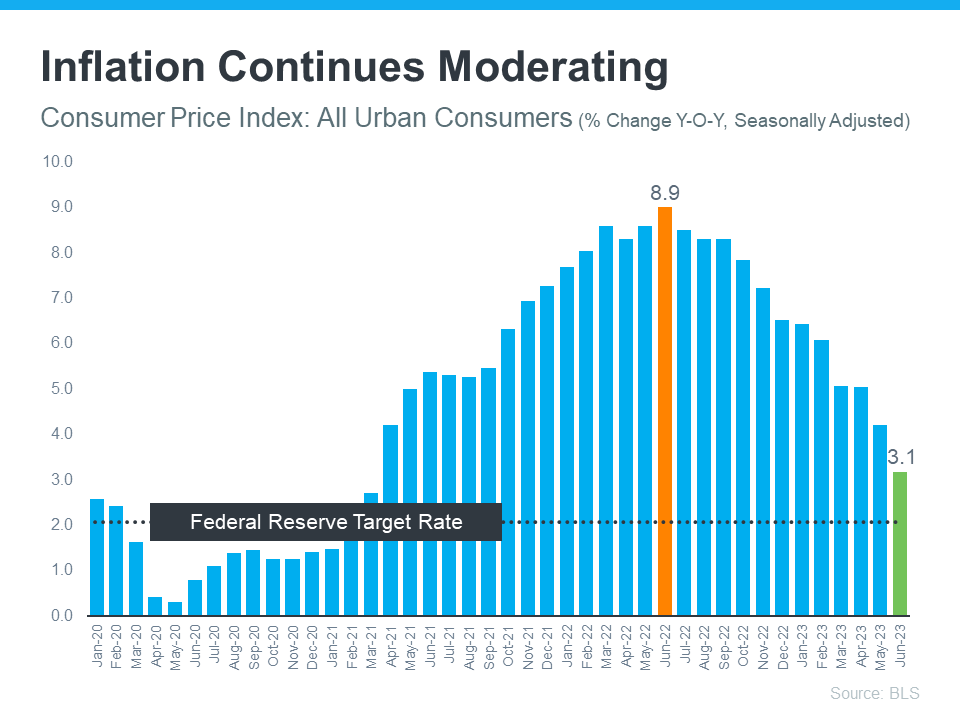

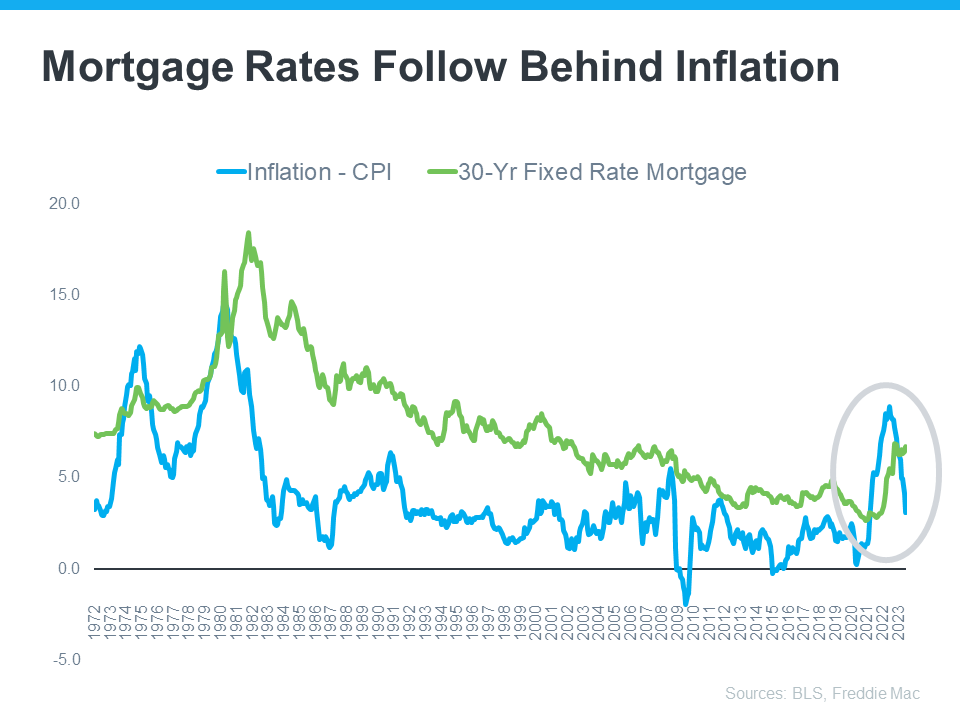

When you read about the housing market in the news, you might see something about a recent decision made by the Federal Reserve (the Fed). But how does this decision affect you and your plans to buy a home? Here's what you need to know. The Fed is trying hard to reduce inflation. And even though there’s been 12 straight months where inflation has cooled (see graph below), the most recent data shows it’s still higher than the Fed’s target of 2%:  While you may have been hoping the Fed would stop their hikes since they’re making progress on their goal of bringing down inflation, they don’t want to stop too soon, and risk inflation climbing back up as a result. Because of this, the Fed decided to increase the Federal Funds Rate again last week. As Jerome Powell, Chairman of the Fed, says: “We remain committed to bringing inflation back to our 2 percent goal and to keeping longer-term inflation expectations well anchored.” Greg McBride, Senior VP, and Chief Financial Analyst at Bankrate, explains how high inflation and a strong economy play into the Fed’s recent decision: “Inflation remains stubbornly high. The economy has been remarkably resilient, the labor market is still robust, but that may be contributing to the stubbornly high inflation. So, Fed has to pump the brakes a bit more.”Even though a Federal Fund Rate hike by the Fed doesn’t directly dictate what happens with mortgage rates, it does have an impact. As a recent article from Fortune says: “The federal funds rate is an interest rate that banks charge other banks when they lend one another money . . . When inflation is running high, the Fed will increase rates to increase the cost of borrowing and slow down the economy. When it’s too low, they’ll lower rates to stimulate the economy and get things moving again.” How All of This Affects You In the simplest sense, when inflation is high, mortgage rates are also high. But, if the Fed succeeds in bringing down inflation, it could ultimately lead to lower mortgage rates, making it more affordable for you to buy a home. This graph helps illustrate that point by showing that when inflation decreases, mortgage rates typically go down, too (see graph below):  As the data above shows, inflation (shown in the blue trend line) is slowly coming down and, based on historical trends, mortgage rates (shown in the green trend line) are likely to follow. McBride says this about the future of mortgage rates:

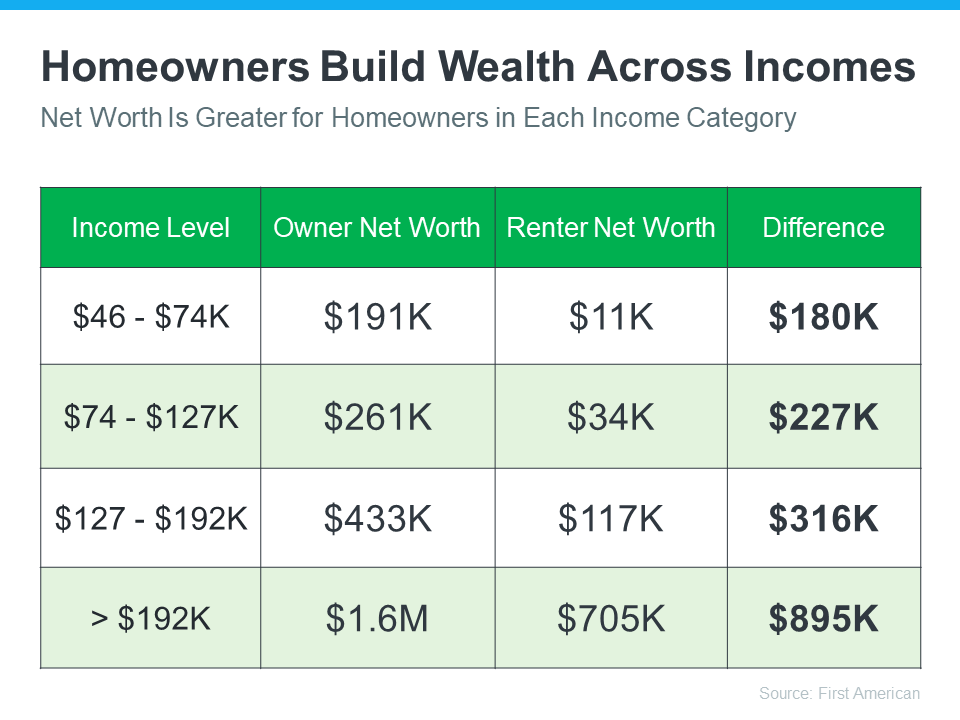

“With the backdrop of easing inflation pressures, we should see more consistent declines in mortgage rates as the year progresses, particularly if the economy and labor market slow noticeably.” Bottom Line What happens to mortgage rates depends on inflation. If inflation cools down, mortgage rates should go down too. Let's talk so you can get expert advice on housing market changes and what they mean for you.  You may have heard some people say it’s better to rent than buy a home right now. But, even today, there are lots of good reasons to become a homeowner. One of them is that owning a home is typically viewed as a good long-term investment that helps your net worth grow over time. Homeownership Builds Wealth Regardless of Income Level You may be surprised to learn homeowners across various income levels have a much higher net worth than renters who make the same amount. Data from First American helps illustrate this point (see graph below):  What makes wealth so much higher for homeowners? A recent article from Realtor.com says:

“Homeownership has long been tied to building wealth—and for good reason. Instead of throwing rent money out the window each month, owning a home allows you to build home equity. And over time, equity can turn your mortgage debt into a sizeable asset.” Basically, the wealth you accumulate when you own a home has a lot to do with equity. As a homeowner, equity is built up as you pay down your loan and as home prices appreciate over time. Mark Fleming, Chief Economist at First American, explains how this same benefit isn’t true for renters in a recent podcast: “Renters as non-homeowners gain no wealth benefit as home prices rise. That wealth actually accrues to the landlord.” Before you decide to sign another rental agreement, now is a good time to think about whether it would be better for you to buy a home instead. The best way to figure out what makes sense for you is to have a conversation with a real estate expert you trust. That professional can talk you through the benefits that come with owning to determine if that’s the right next step for you. Bottom Line If you're not sure whether to keep renting or to buy a home, know that owning a home, no matter how much money you make, can help build your wealth. Let's connect now to get started on the path to homeownership. |

BLOG Archives

April 2024

|

|

The Big City Team

Berkshire Hathaway HomeServices 6416 Bay Parkway, 2nd floor Brooklyn, New York 11204 Colin R. O'Leary Founder & Team Leader Licensed R.E. Salesperson Phone: 646-300-2012 Email: colinoleary@bhhsfillmore.com |

|

Your Trusted Partners in Real Estate Across the NYC Metro Area

© 2024 BHH Affiliates, LLC. An independently owned and operated franchisee of BHH Affiliates, LLC.

Berkshire Hathaway HomeServices and the Berkshire Hathaway HomeServices symbol are registered service marks of Columbia Insurance Company, a Berkshire Hathaway affiliate.

Equal Housing Opportunity.

Privacy Policy